Digital Credit Union

Digital Credit Union (DCU) is the largest credit union in New England and in the top twenty nationwide. This is largely due to word-of-mouth and member loyalty. Because credit unions are employee- or member-owned, member-centricity had always been core to DCU’s culture. But, despite a long track record of delivering excellent in-person service, the results were proving uneven in a digital-first world.

21 actionable opportunities surfaced across 4 themes · Behavioral personas anchored in member mental models and goals · A digital onboarding "secret shopper" exercise the research team was unable to complete

Fierce Loyalty at Risk

Despite often exemplary in-branch service, the transition to a digital-first world was not going well for DCU. Online banking worked well enough, but there were serious issues within the customer journey. Take member onboarding:

My team spent thirty days trying to open a Digital Credit Union account. Not as a member but as researchers mapping the new member digital onboarding journey through a “secret shopper” exercise. We started by trying to open an account for a spouse. After multiple failures—an excessive document upload that ended with “I'm not eligible? Or am I?,” an authentication loop that wouldn't resolve, a chatbot that asked whether we were existing customers and then disagreed with our answer—we gave up on that account and tried to open another one. After about thirty days, we gave up that one too. DCU has a funded account that we were never able to log in to use. The experience encapsulated an urgent case for change.

Digital Credit Union grew to become the largest credit union in New England (and one of the top twenty nationwide) on word of mouth and fierce member loyalty, loyalty won from authentic personal service from people who actually recognize you. It’s the kind of service that arises from being mission-driven and from having employees passionately dedicated to that mission. It’s an advantage most banks can only dream of. Indeed, it’s a precious, hard-won advantage that’s impossible to fake because that kind of personalized service takes time, care, and dedication to create and sustain.

Yet, for DCU, that advantage was at risk because it wasn’t working beyond the branch threshold. In the digital channel where people increasingly did their banking, the experience DCU delivered expressed none of the hallmarks that long-time, loyal customers noted had won DCU their business for life. Only 36% of members considered DCU their primary financial institution.

The things that had historically drawn customers closer to DCU were not just absent in the digital experience, the experience was actually pushing potential customers away. And the opportunity went beyond copying other bank’s online tools. DCU had something unique that could transform what a digital banking experience could be.

Gradually, and Then Suddenly

In Hemingway's The Sun Also Rises, a character is asked how he went bankrupt. “Two ways,” he replies. “Gradually, and then suddenly.” At the time of the engagement, digital-first disruption had been gradual for a decade and was accelerating. The credit union sector had not yet hit the suddenly.

Core to the strategy, then, were three risks that every financial institution needed to address:

Digitization: Online services have made it easier than ever for customers to find, compare, and switch among financial products. Open banking was raising the bar for what a digital experience needed to do to extend the relationship a financial institution may otherwise have created in person within their geographic region.

Commodification: Customers always expect value when it comes to their money, but competing primarily on rate is a race to the bottom no member-owned institution should run. If an institution can instead offer integrated solutions tied to key points in a customer’s financial lives, rather than standalone products competing on price, they would have a durable competitive advantage.

Experience Management: As members encounter a wider set of national and digital-first competitors, journey management—the discipline of designing how a member moves through their relationship with the institution over their lifetime—becomes increasingly central to both retention and growth.

The Work

The question DCU brought to us was how to carry its member-first ethos, frequently delivered in-branch, into a digital channel where younger generations increasingly form their financial habits, and where national and digital-first competitors were setting new expectations for what an online banking experience could be.

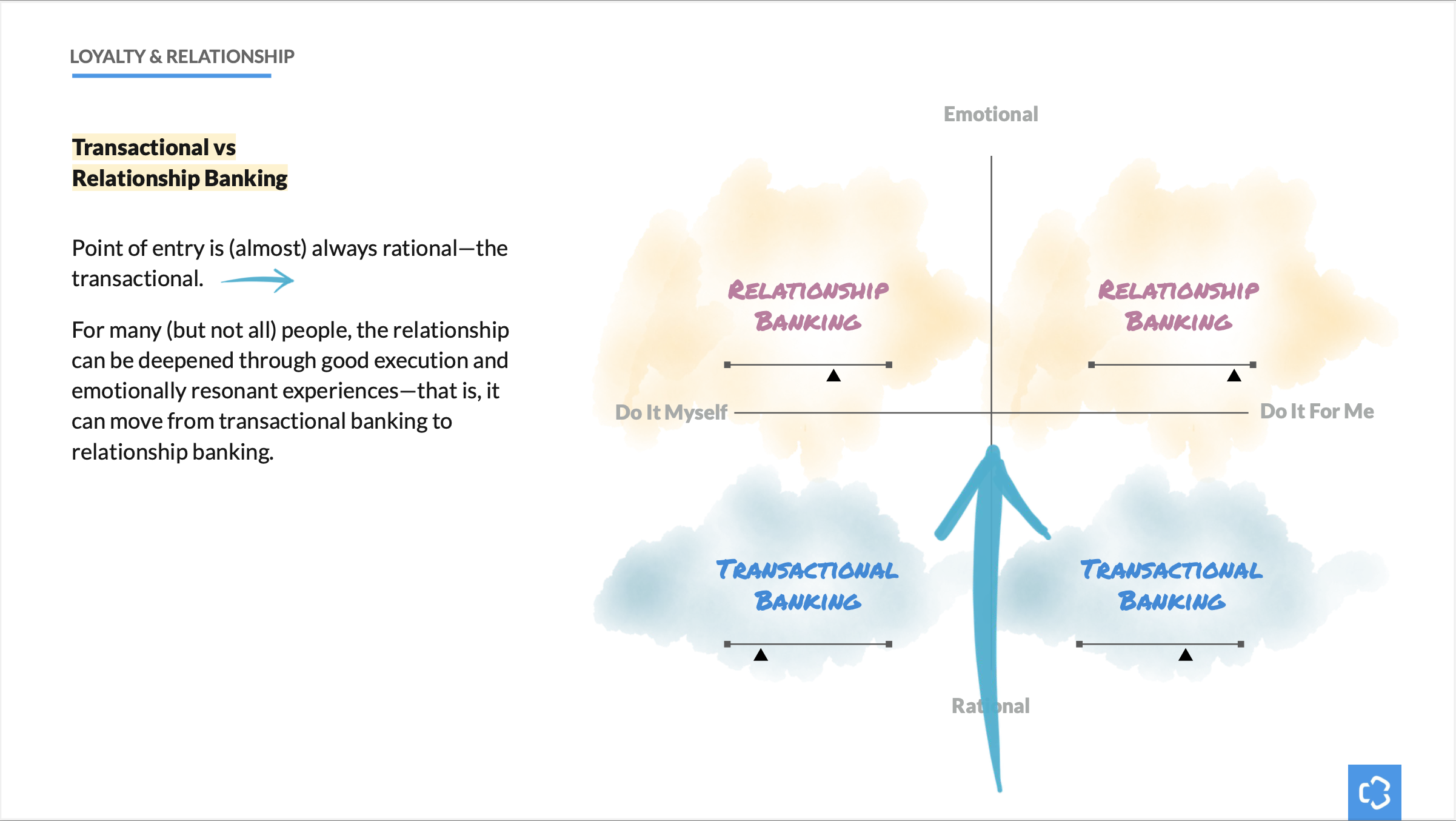

I partnered with DCU to translate its strong in-person ethos into the digital channel through ethnographic member-insights research. The work identified 21 actionable opportunities across four themes and produced a set of behavioral personas—distinct ways members think about and engage with money—that gave DCU a more granular way to segment member journeys and personalize the digital experience around how members actually behave, not just who they demographically are.

The work surfaced the gap between DCU's member-centric culture and its operating reality, an organization founded on member-centricity but not yet structured to translate member insight into digital experience. While each opportunity offered a point a leverage, a change that could alter the member experience and resulting lifetime value, a comprehensive approach to design would be needed. The concrete action we recommended was for DCU to build the design-enablement discipline necessary to translate the insights into shipped change, change at the scale that a DCU member deserved.

Research uncovered different thinking styles that could be leveraged both to personalize the banking experience and to drive growth and customer satisfaction through the application of targeted Key Experience Metrics (KEIs.). This is one slide from a 90 screen research findings deck.

Behavioral personas synthesized distinct thinking styles and attitudes toward money. They allowed DCU to personalize CX and product offerings to engage more potential members.

The Recommendation

To paraphrase Eisenhower, research alone is useless, but research is also indispensable. Based on our prior engagement, DCU already had enough insight to act. What it needed was the operational discipline to act on what it had learned.

We recommended three coordinated actions:

Design Enablement: Training DCU's people in design thinking and design doing, so the entire organization could work from member insights rather than business-line assumptions.

Design Delivery: Working in partnership with DCU's existing Experience Design Team to prototype and ship the highest-value member-facing solutions to prove out the strategy, thereby building credibility for further investment.

Executive Alignment: Building the cross-silo governance and metrics that would let journey management actually take root, because top-down change and bottom-up energy are both needed to complete a transformation.

Unfortunately, DCU did not commission the extension. As sometimes happens, the work ended at the diagnosis. Insights are always at risk of being nothing more than ideas sitting on a shelf.

The Takeaway

DCU had created something enviable: fierce loyalty earned from authentic, personalized service impossible for competitors to easily copy. Its foundation was its member-owned mission and the consistent bright spots delivered to members in-branch and over the phone. But member-centricity doesn't automatically translate into a digital channel, or scale across channels as the institution grows. It has to be explicitly designed, culturally, operationally, and in how the organization measures whether it's actually delivering it.

Strategic research is useful in helping an organization see both its challenges—and opportunities—clearly. But knowing is valueless without action. What converts seeing into doing is the design-enablement discipline that yields cross-silo journey management, member-centered metrics focused on financial well-being, and the cultural capacity to continually build on what the research surfaced.

Next time you’re tempted to design first without understanding the customer and their lived context, take a step back and do the research. Once you’ve done the research, don’t let it go to waste; realize instead that design and research are two sides of the same coin.

Research explained the “why” behind people’s attitudes, beliefs, motivations, and behaviors.

Role

Strategist

Researcher

Service Designer

Key Deliverables

Strategic Recommendations

Member Personas

Digital “Secret Shopper” CX Analysis